The Global Currency MeltdownAny sharp decline of rupee, from current levels however, unlikely

KEY TAKEAWAYS

- Currency depreciation and volatility vis-à-vis the US dollar has been as widespread and pervasive across the countries of the world in H12022 as the Covid pandemic itself.

- Simultaneous interplay of multiple headwinds such as lingering geopolitical conflicts, elevated commodity price pressures and a concurrent monetary policy tightening across the major economies have all played a role in the rise of the dollar.

- The dollar index has appreciated by nearly 10% since the start of 2022 with a combination of high inflation in US and global risk aversion driving the demand for the world’s primary reserve currency.

- US Federal Reserve has already hiked interest rates by 150 bps in 2022 and is expected to raise rates by another 200 bps during the remaining months of 2022. Cumulatively, this would be tantamount to about 350 bps rate hike during 2022, making it the most aggressive rate hike cycle since the Volcker era. Additionally, the Fed has also begun quantitative tightening (QT) which will intensify the impact of monetary policy normalization and provide a supplementary tailwind to the USD.

- While the INR has depreciated by 7.3% against the dollar in 2022 so far, interestingly, the rupee has appreciated against many other DM currencies during the same period such as the Euro, GBP, and the Yen.

- The near term outlook for INR will continue to remain uncertain given the persistent volatility in the global markets but with the likely moderation in commodity prices and a potential reversal of the large capital outflows, any sharp decline from the current levels of 80/USD is unlikely.

Ascendant dollar weighs down currencies globally

INR likely to stabilize in the band of Rs 79-81 by Mar-23

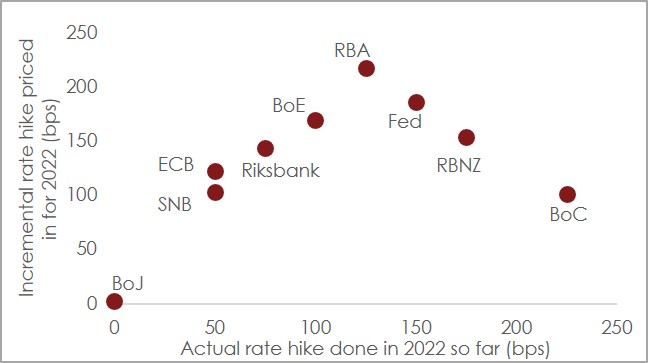

Significant volatility in forex market has become a dominant theme across economies amidst simultaneous interplay of multiple headwinds such as lingering geopolitical conflicts, elevated prices pressures, and a concurrent monetary policy tightening across the major economies. Such high volatility was last seen during the onslaught of the pandemic during 2020. The turn in global monetary policy has gathered steam, with US Fed leading the pack in normalizing interest rates aggressively (Chart 1) thereby triggering the safe haven demand for the US dollars and causing persistent depreciation in all other currencies.

Chart 1: Fed remains the most hawkish DM central bank

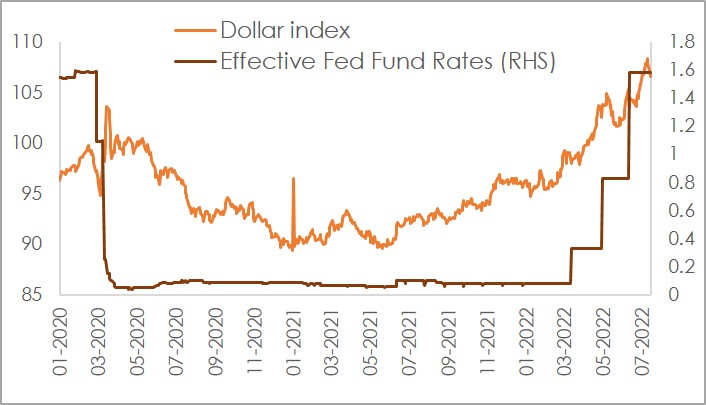

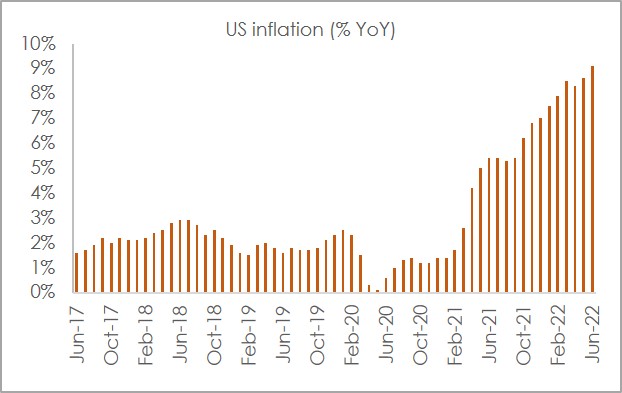

The dollar index has appreciated by nearly 10% since the start of 2022 with a combination of high inflation (Chart 9, Annexure) and geopolitical instability driving the demand for the world’s primary reserve currency. The USD is further expected to continue deriving support from aggressive interest rate hikes and monetary tightening in the US along with geopolitical led risk aversion (Chart 2).

Chart 2: Rise in interest rate increases the USD appeal

High and persistent inflation has imparted a sense of urgency to monetary policy normalization by the US Fed. After hiking monetary policy rate by 150 bps so far in 2022, the US Federal Reserve is expected to hike interest rates by another 200 bps during the remaining months of 2022. Of this, there is a strong likelihood of 75-100 bps hike getting executed in the upcoming FOMC policy review in July. Cumulatively, this would be tantamount to about 350 bps rate hike during the calendar year 2022, making it the most aggressive rate hike cycle since the Volcker era. Additionally, the Fed has also begun quantitative tightening (QT) to further address inflation risks. The monthly pace of QT will involve USD 47.5 bn selling of securities (USD 30 bn USTs and USD 17.5 bn Agency MBS) before raising it further to USD 95 bn in Sep-22 (USD 60 bn USTs and USD 35 bn Agency MBS). The wind down of the Fed balance sheet will reinforce the impact of monetary policy normalization and would provide a supplementary tailwind to the USD.

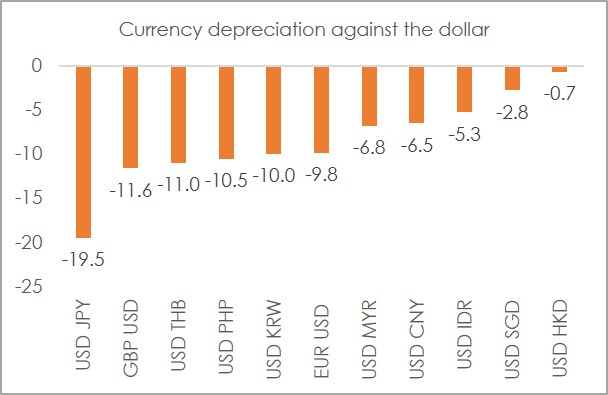

Given the extraordinary accommodative policies rolled out during the pandemic by the developed economies (DMs) along with the lingering supply chain bottlenecks, these economies have been facing higher inflationary pressures than the emerging economies (EM), leading many hard currencies such as the Yen, GBP and EUR to depreciate significantly against the dollar in the current calendar (Chart 3).

Chart 3: DM currencies record higher depreciation

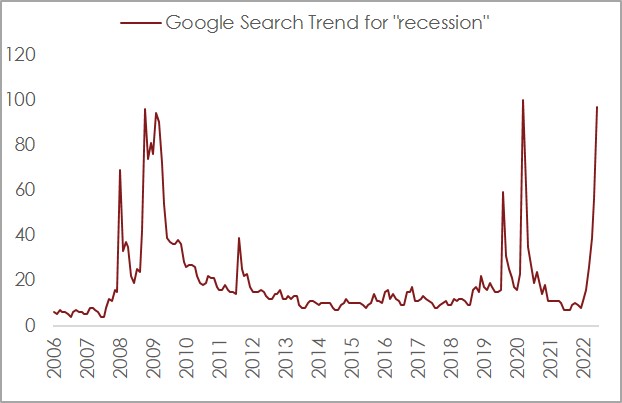

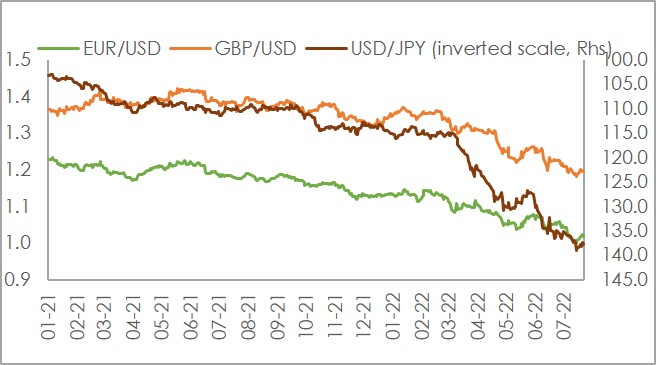

Yen has depreciated at an unprecedented pace of 19.5% in 2022 so far. The primary reason for Yen’s significant decline is the divergence in monetary policies of Japan and the US, leading the interest rates differentials between the two countries to widen. In the recent policy decision, Bank of Japan (BoJ) continued to remain an outlier in the era of global central bank policy tightening cycle. While it raised its inflation forecast, the BoJ maintained its ultra-low interest rates underscoring concerns over the fragile growth scenario. While rising fuel and commodity costs have pushed Japan’s inflation above its 2% target, the BoJ has repeatedly said that it was in no rush to withdraw stimulus as slowing global growth cloud the outlook for the still-weak economy. With BoJ being the lone major central bank adhering to an accommodative policy, the Yen is at risk of weakening further against the dollar for at least the rest of 2022. GBP in 2022 so far has depreciated by 11.6% on the back of deteriorating economic outlook amidst elevated inflation level, higher cost-of-living, stalling growth scenario and ongoing Brexit woes. On the other hand, while EUR has been currently trading at 1.02 against the USD, recently the currency had dropped below the psychologically important parity level against the USD for the first time in nearly twenty years. Going forward, while the delivery of extreme hawkish rhetoric by the ECB (raised interest rates by 50 bps after 11 years) would help support the currency to some extent, the intensifying recessionary fears (Chart 4) on the back of rising uncertainty about energy supply to the bloc is expected to lead the depreciation bias to continue.

Chart 4: Increasing fears of recession to keep USD demand high

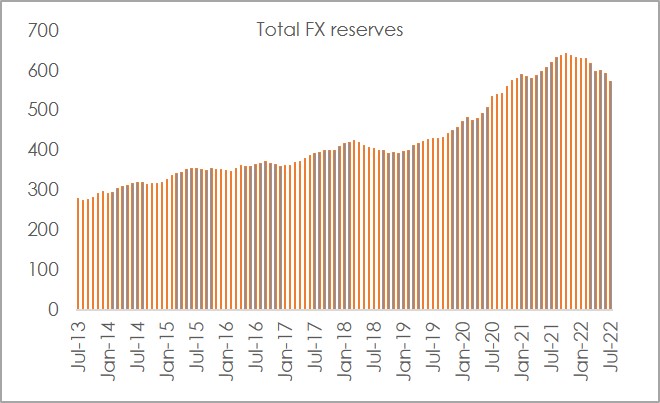

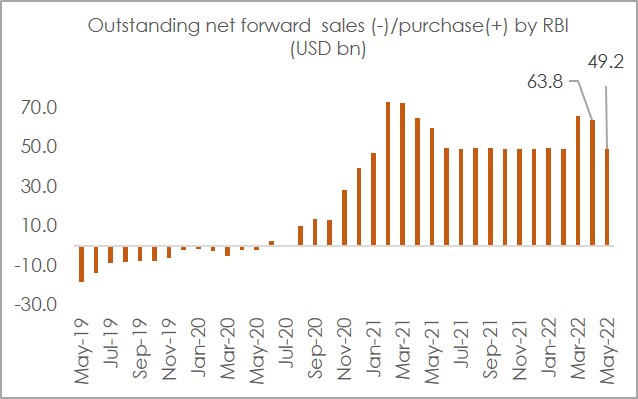

While the emerging market currencies do not remain unscathed from the persistent strength in the USD, the INR seems to be better placed than most of the EM currencies such as South Korean Won, Philippines Peso, and Thai Baht. The continued intervention by the central bank in the spot market (leading the FX reserves to decline) and the forward market segment (Chart 12) has helped the rupee to keep its losses capped. As per the latest data, RBI’s FX reserves have fallen to USD 572.7 bn as on mid-July’22 from USD 593 bn as the end of Jun-22 (Chart 5). Although it’s still comfortable and will continue to provide the first line of defence against excessive volatility in INR, the overall import cover is slowly moderating (from its peak of over 19-months of in early 2021 to nearly 10 months currently).

Chart 5: RBI intervention moderates its reserves position

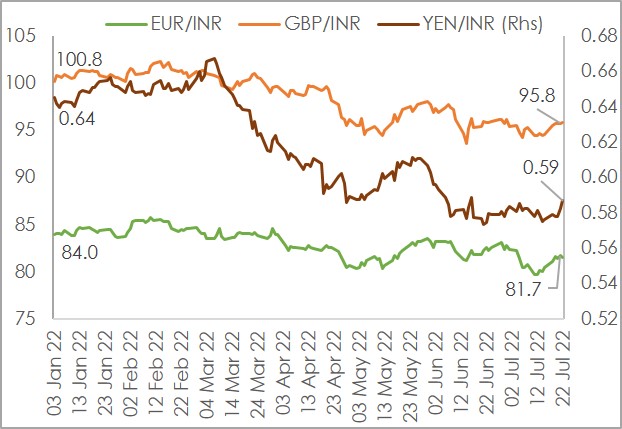

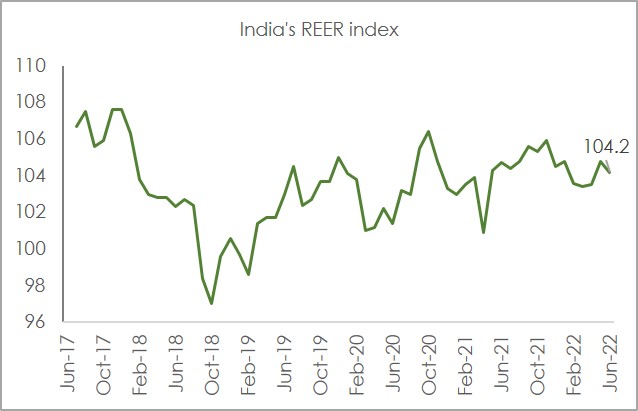

Interestingly, the rupee has appreciated against many other currencies during the same period such as the Euro (2.7%), GBP (4.9%), and the Yen (4.9%) (Chart 6). Consequently, India’s trade-weighted Real Effective Exchange Rate (40-country REER, Base: 2015-16=100) remained around 104 in June (Chart 13).

Chart 6: INR has actually appreciated against EUR, GBP and YEN

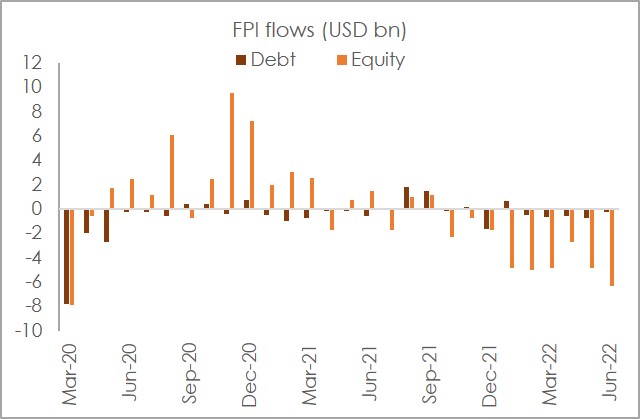

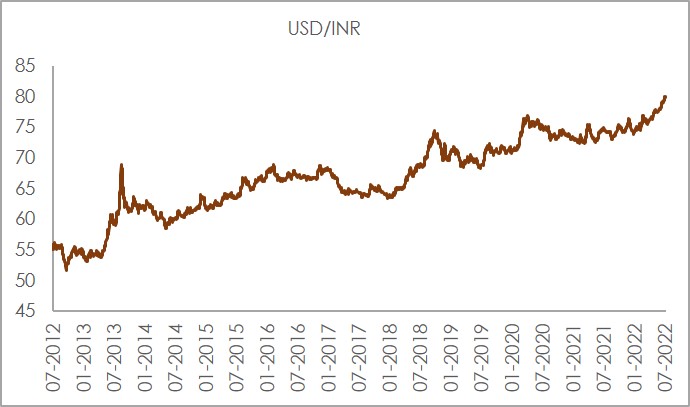

That said, monetary policy tightening globally, and consequent portfolio outflows (Chart 7) has been the primarily reason for the persistent weakness in the Indian rupee over six consecutive months and culminating into a depreciation of 7.3% in 2022 so far (currently at 79.8 against the USD, gaining marginally after breaching the 80 level) (Chart 8).

Chart 7: Portfolio outflows stands at USD 30.5 bn in 2022 so far

The last time rupee saw six consecutive months of weakness was during the backdrop of the domestic NBFC crisis in 2018. Monetary policy tightening by the US Fed was nevertheless a common underlying factor between the 2018 episode of consistent weakness in rupee as well as the current ongoing phase of depreciation.

Chart 8: INR has in 2022 has so far depreciated by 7.3%

INR Outlook:

INR Outlook: Looking at the current scenario, the broad theme driving rupee weakness has continued to remain intact for the last 6-7 months. We continue to believe that there is room for further weakness, albeit to a moderate extent.

The pressure on India’s BoP has been escalating since Q4 FY22. Monthly trade data for Q1 FY23 shows a significant expansion of the merchandise deficit to a record high level of USD 70.9 bn. Together with USD 14.4 bn portfolio outflow during the quarter, the Net BoP position could turn out to be in the USD 15-20 bn deficit range. Any extrapolation of such a quarterly BoP trend for the remaining three quarters would make the full year (FY23) picture appear ominous. While we continue to expect FY23 BoP to post a sizeable deficit of USD 33 bn, size of the deficit could potentially moderate in the coming quarters due to the following factors:

- Most commodity prices have corrected significantly in last 3-4 weeks on account of growing concerns of a global hard landing (led by the US and Chinese economy). The Reuters CRB Commodity Index has fallen by ~10% on monthly average basis in Jul-22, registering its first monthly decline in 2022 so far. This could provide moderate relief to India’s trade deficit in the coming months. Nevertheless, with crude oil prices expected to average in the range of USD 105-110 pb, along with elevated demand for imports and moderating exports, we expect FY23 current account deficit to widen to around USD 105 bn (~2.9% of GDP).

- While portfolio outflow has persisted for tenth consecutive month, the magnitude has tapered considerably with Jul-22 registering a meagre outflow of USD 0.1 bn so far. We believe the sentiment could stabilize somewhat in the coming months as inflation peaks out in US and correction in asset prices provide opportunities for churning the investment portfolio.

- Recently, the RBI has also announced a series of steps to augment capital inflows in the near term.

- With an aim to incentivize NRI deposits, the central bank granted CRR and SLR exemption to banks (on incremental FCNR(B) and NRE term deposits) up to Nov 4, 2022. In addition, banks have also been permitted to raise fresh deposits (FCNR(B) and NRE) without reference to extant regulations on interest rates - this relaxation will be available up to Oct 31, 2022.

- Further, to incentivize debt investment by the FPI and to increase the choice of G-secs available for investment by NRI, the central bank has now expanded the FAR (Fully Accessible Route) basket to include all new issuances of 7Y and 14Y g-secs from an access of just 5,10 and 30 year tenors earlier. In addition, limits on short term investments (in securities with residual maturity of less than 1Y) in g-secs and corporate bonds have been exempted until Oct 31, 2022. Further, investment in corporate money market instruments with original maturity of up to 1Y can now be done (up till Oct 31, 2022), with such investments to be treated as outside reckoning for considering the short-term limit for investments in corporate securities.

- In a move to promote global trade and to support increasing global interest in rupee, the RBI announced a mechanism to settle tractions in rupee terms. While in the short run this reform is not expected to lead to any immediate surge in rupee trade settlement, in the long run internationalization of INR could help to reduce the demand for dollars, cap large-scale depreciation pressures for the rupee and help preserve forex reserves.

That said, we believe that INR could continue to carry a mild depreciation bias as (i) exchange rate adjustment would be a natural stabilizer for expansion of the current account deficit, and (ii) excessive use of reserves to curb depreciation pressures amidst the backdrop of broad-based dollar strength would increase INR’s real effective overvaluation vis-à-vis peers.

To conclude, Acuité believes that the INR may stabilize in the band Rs 79-81 by March 2023 with the expected moderation in commodity and crude oil prices and the prospects of some reversal of the sharp capital outflows seen over the last six months.

Annexure: Supplementary graphs and charts

Chart 9: US Inflation highest at 9.1% since 1981

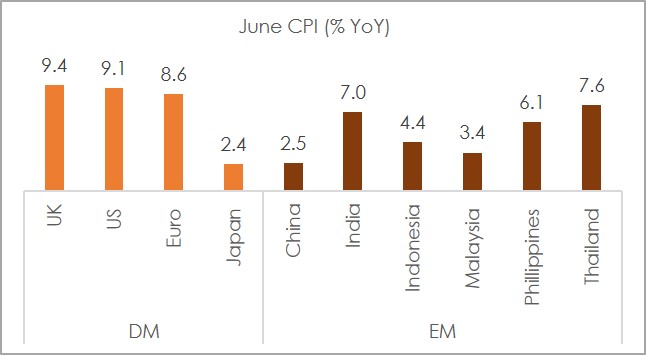

Chart 10: DMs face higher inflation than EMs

Chart 11: Trend of depreciation in hard currencies

Chart 12: Total drawdown of USD14.36 bn from RBI’s forward book in May-22

Note: The forward book position of the RBI comes with a log of 2 months

Chart 13: India’s REER remained overvalued at 104.2 in June-22

Note: All data for the graphs and charts in this article have been sourced from CMIE, RBI and other sources in public domain

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD