KEY TAKEAWAYS

As per the final estimates, India’s merchandise trade deficit widened to USD 20.1 bn in Apr-22 from USD 18.5 bn in Mar-22. While both exports and imports moderated sequentially in Apr-22, the relatively larger drop in exports resulted in expansion of the trade deficit.

Exports: Moderates in line with seasonality

In value terms, merchandise exports moderated to USD 40.2 bn in Apr-22 from its record peak level of USD 42.2 bn in Mar-22. This translates into a sequential contraction of 4.8% MoM and is typically in line with seasonality seen in April after year end volumes in Mar-22.

Imports: A mixed picture

Merchandise imports posted a mild moderation to USD 60.3 bn in Apr-22 vis-à-vis its all-time high monthly level of USD 60.7 bn in Mar-22, translating into a sequential growth of -0.7% MoM. At a granular level:

Outlook

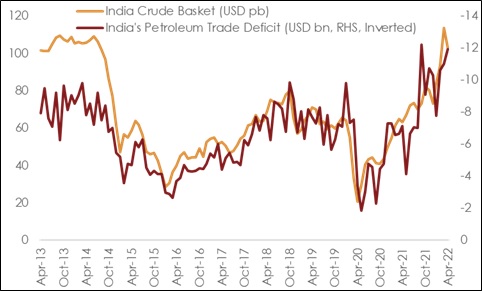

The expansion of trade deficit in Apr-22 is in line with the seasonal trends. In addition, higher petroleum deficit also continues to play a role. The steady buildup of petroleum deficit in last 3-months is on the back of sharp acceleration in international crude oil prices triggered by the Russia-Ukraine conflict.

The geopolitical crisis continues unfettered for the third consecutive month, keeping global commodity prices elevated. While the ongoing conflict is likely to dampen world trade volume (the IMF downgraded its estimate for 2022 world trade volume growth to 5.0% in Apr-22 from 6.0% estimated earlier in Jan-22), the price impact could offset the volume impact.

We believe this trend to manifest clearly in case of India’s exports in FY23. Further, the buildup of recent momentum, evolving global geopolitical dynamics (diversification of global value chains from China and Russia/Ukraine markets), and policy support through targeted incentive structures like the PLI Scheme and bilateral trade deals would drive a structural growth in exports, besides the inorganic expansion via price effect. Nevertheless, some normalization in growth is likely in the coming quarters on deceleration in global demand.

With India being a net importing economy, the commodity price effect could be larger (as of date, the Reuters CRB Commodity Index is 34% up compared to its average level in FY22) for imports. In addition, unlocking of the domestic economy post the Omicron wave along with vaccination drive gaining critical mass (with 63% of the population having received double dose) is expected to drive domestic demand for imports including the pent up factor.

As such, we continue to expect India’s current account deficit to widen towards USD 85 bn in FY23 from an estimated level of USD 44 bn in FY22. However, there is a risk to our estimate which stems from the current bout of unusually high degree of volatility in global commodity prices.

The rupee continues face depreciation pressures vs the USD and also exhibit volatility due to the geo-political crisis, increased capital outflows sparked by increasing interest rates in developed economies and not the least, the significant increase in trade and current account deficit that is already visible for the current year.

It may be noted that India’s gross reserves have declined from USD 633.6 bn as on Dec 31, 2021 to a current level of USD 595.9 bn as on May 6, 2022, reflecting the heightened pressures on the INR. It has not only breached the level of 77.0 but may also breach 78.0 in the short term if the capital outflows continue unabated.

Table 1: Highlights of merchandise trade balance

| India's merchandise trade highlights (USD bn) | ||||

| Apr-21 | Mar-22 | Apr-22 | FY22 | |

| Exports | 30.8 | 42.2 | 40.2 | 419.7 |

| Oil Exports | 3.6 | 7.8 | 8.3 | 60.5 |

| Non-oil exports | 27.1 | 34.4 | 31.9 | 355.9 |

| Imports | 46.0 | 60.7 | 60.3 | 611.9 |

| Oil imports | 10.8 | 18.8 | 20.2 | 164.3 |

| Gold Imports | 6.2 | 1.0 | 1.7 | 46.2 |

| NONG imports | 29.0 | 40.9 | 38.4 | 398.5 |

| Trade Balance | -15.3 | -18.5 | -20.1 | -192.2 |

Chart 1: Escalating oil prices are weighing on India’s petroleum trade deficit

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD