KEY TAKEAWAYS

India’s merchandise deficit perceptibly narrowed to an 8-month low of USD 6.3 bn in May-21 from USD 15.1 bn in Apr-21. The moderation in trade deficit was led by a sequential increase in exports (+5.4% MoM) along with a significant sequential decline in imports (-15.7% MoM). We had already highlighted in our May-21 edition of "Acuite Macro Pulse” about the possibility of a sharp compression in May-21 trade deficit on account of state level lockdowns getting pervasive even as India’s key export partners progressively relaxed lockdown restrictions in their respective countries.

Looking at the drivers of trade deficit in May-21, we find that:

Exports: Remain healthy

In value terms, exports improved moderately to USD 32.3 bn in May-21 (+69.4% YoY due to the sheer base effect) from USD 30.6 bn in Apr-21. At a granular level:

Imports: Disruption from Covid

Merchandise imports slipped to a 6-month low of USD 38.6 bn in May-21 (+73.6% YoY) from USD 45.7 bn in Apr-21. At a granular level:

Outlook

There are two key trends critical for India’s trade deficit. In the near term, the overhang of Covid disruption could potentially persist for another month with Jun-21 trade deficit printing at moderate levels (could be around USD 11-12 bn, but wider on account of gradual relaxation in state level lockdowns, especially in the second half of Jun-21). This will ensure that India’s Q1 FY22 current account balance switches to a moderate surplus, like Q1 FY21, albeit to a much lesser degree.

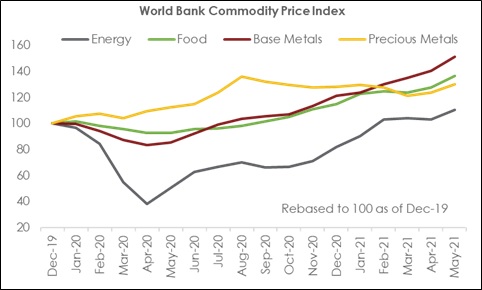

However, the current account surplus is unlikely to sustain as global commodity prices have hardened considerably in last two quarters, to above pre Covid levels in most cases. More importantly, with the second wave ebbing, states have started to taper their lockdown stringency. This should once again start supporting overall economic activity, which would further get a boost from anticipated ramp up in domestic vaccination drive in the coming months. Hence, we continue to stick to our FY22 current account estimate of approximately USD 30 bn deficit vis-à-vis USD 26 bn estimate in FY21.

Table 1: Key items within merchandise trade balance

| India's merchandise trade highlights (USD bn) | ||||

| May-20 | May-21 | Apr-May FY21 |

Apr-May FY22 |

|

| Exports | 19.1 | 32.3 | 29.4 | 62.9 |

| Petroleum Exports | 1.6 | 5.3 | 2.9 | 9.0 |

| Gems & Jewellery Exports | 1.1 | 3.0 | 1.1 | 6.3 |

| Core Exports | 16.4 | 24.0 | 25.4 | 47.6 |

| Imports | 22.2 | 38.6 | 39.3 | 84.3 |

| Petroleum Imports | 3.5 | 9.5 | 8.1 | 20.3 |

| Gems & Jewellery Imports | 0.8 | 2.9 | 0.9 | 11.7 |

| Core Imports | 17.9 | 26.2 | 30.3 | 52.3 |

| Trade Balance | -3.2 | -6.3 | -9.9 | -21.4 |

| Petroleum Trade Balance | -1.9 | -4.1 | -5.3 | -11.4 |

| Gems & Jewellery Trade Balance | 0.3 | 0.0 | 0.2 | -5.3 |

| Core Trade Balance | -1.6 | -2.2 | -4.8 | -4.7 |

Chart 1: Global commodity prices have seen a sharp run up in last 2-quarters

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD