KEY TAKEAWAYS

In its’ bi-monthly review held between Oct 6-8, 2021, Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI) maintained status quo on rates in line with expectations. As such, the Repo, Reverse Repo, and Marginal Standing Facility rates remained unchanged at 4.00%, 3.35% and 4.25% respectively; in a 6-0 unanimous vote. In addition, the MPC also decided to continue with the ‘accommodative’ stance ‘as long as necessary in a bid to support growth on a durable basis’, in a 5-1 vote with Prof. Jayanth R. Varma expressing dissent once again.

Economic Assessment

Growth: MPC retained its FY22 growth forecast at 9.5%, citing continued traction in domestic economic activity. On the demand side, RBI expects rural economy amidst normal Kharif sowing and bright Rabi prospects to remain at the vanguard of private consumption. The progress on vaccination and the onset of festive season is likely to buoy urban consumption, especially for services. On the supply side, Government reforms on asset monetization and infrastructure development along with those focused on telecom and banking sectors, are likely to crowd in private investments.

On the downside, the MPC did highlight possible risks from global semi-conductor shortages, elevated commodity prices and potential global financial market volatility, along with continuing uncertainty around prospects of another Covid wave.

While aggregate demand is improving, RBI did admit to some slack remaining in the economy with output yet to catch up with the pre-pandemic level – perhaps, serving as a justification for the accommodative policy stance to continue.

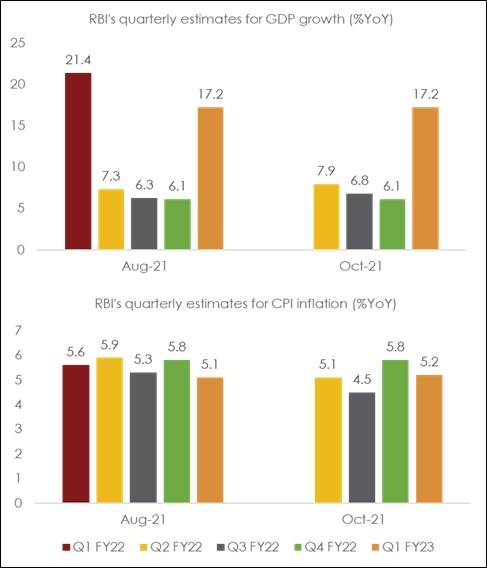

On a quarterly basis, after the 20.1% expansion in Q1 FY22, RBI projects real GDP growth over the remaining three quarters at 7.9% in Q2 (upped from 7.3%), 6.8% in Q3 (upped from 6.3%) and 6.1% in Q4 (see chart).

Acuite continues to expect FY22 GDP growth at 10.0%, albeit with some downside risk due to raw material shortages in some sectors and higher commodity prices.

Inflation: In a surprise move, RBI lowered its FY22 CPI inflation projection by 40 bps to 5.3%. This appears to have been prompted by the significant moderation in CPI inflation over the months of Jul-21 and Aug-21 (and also anticipated for Sep-21), along with a benign near-term outlook based on (in addition to a favorable base) –

The downward revision comes despite India’s crude basket on an average hardening, currently at USD 79 pb compared to USD 70 pb at the time of the last policy in early Aug-21. In addition to pressures from higher crude oil prices, RBI did acknowledge rising metal and energy prices, shortage of industrial components and high logistics costs adding to cost push inflation.

On balance, RBI projects CPI inflation at 5.1% in Q2 (lowered from 5.9%), 4.5% in Q3 (lowered from 5.3%) and 5.8% in Q4 FY22.

While softer food inflation expectations on the back of a healthy kharif crop may have prompted RBI to lower its inflation estimate to 5.3% for FY22, we would attach an upward bias to this forecast given elevated global prices across the categories of food, energy, metals, and freight along with shortages in industrial raw materials.

Chart 1: Revised GDP and CPI inflation estimates from RBI for FY22

Liquidity and Credit Measures

Outlook on monetary policy

The Governor in his policy address drew a parallel between monetary policy normalization with that of a yet to be anchored boat. He said that "as we are approaching the shore, when the shore is so close, we don't want to rock the boat, because we realise there is a life, there is a journey beyond the shore." This reiterates RBI’s approach of ‘gradualism’ i.e., sans any surprises towards policy normalisation.

In terms of outcome of the announced policy measures, the intended calibration of liquidity (viz. discontinuation of GSAP and higher VRRRs) is likely to adjust short term money market rates gradually upwards in the policy rate corridor. We believe this is a precursor to interest rate normalization. While we stick to our assumption of normalization of the LAF corridor width via hike in reverse repo rate in Dec-21, the likelihood of its postponement onto next quarter is on the rise given RBI’s more gradual approach towards policy normalization. In terms of the timing, this is likely to happen only after US Federal Reserve’s implementation of taper plans from Nov-21.

From G-sec perspective, we continue to expect some hardening in the 10Y g-sec yield towards 6.50% by Mar-22. Having said so, the yield curve is likely to flatten as shorter end of the curve will probably see greater upward adjustment with normalization of monetary policy. The upside in the 10-year yield may however be capped from the possibility of India’s inclusion in the global bond indices in CY22 and the recent change in sovereign rating outlook by Moody’s from ‘negative’ to ‘stable’. We believe the presentation of FY23 Union Budget in Feb-22 would throw some light on this matter.

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD