Sharp drop in passenger load factor, air fares to lead to short-term financial stress

Covid-19 or the Corona Virus has dealt a significant blow to the global economy. The virus outbreak which was first reported in China in mid-December, has assumed the proportion of a pandemic and as per last count, 1.7 lakh people have been infected worldwide across 110 nations with over 6,500 deaths. Beyond China, the impact of Covid-19 has been most severe in Italy, Iran, South Korea, Spain, Germany, France and USA but is rapidly spreading to other parts of the globe. In order to arrest the spread of the pandemic, governments across the world are taking measures involving declaration of emergency or lockdown. This has already led to large scale economic disruption and has induced a significant revision in global growth forecasts for CY2020 from the earlier level of 2.9% to 2.4% with fears of recession in some of the developed nations. (OECD) Expectedly, this will have a substantial impact on the Indian economy which has been witnessing headwinds from a domestic demand slowdown. While the number of infected people in India is still relatively low at around 100 and the mortality is yet to pick up, the risks of its spread across the country are high given the size of the population, the general level of awareness and the inadequate availability of quality healthcare.

The disruption in general economic activity including supply, production, operation and sales will clearly impact the near term outlook for a wide range of industries in India. Acuité believes that the primary and immediate impact will be seen in the services sector i.e. travel, hospitality and retail in that order. While the extent of the impact will depend on the duration of the virus risk, it is clear that there will be a very sharp near term adverse effect on the travel segment and particularly the aviation sector in India.

There has already been a drastic impact on the global aviation industry since the outbreak in China in January 2020. Thousands of flights have already been cancelled by international airlines in Feb-March and much more are on the way over the next 1-2 months, given the travel restrictions and quarantine requirements that are being put in place by an increasing number of nations. With the rapid spread of Covid-19 across Europe, US has put an embargo on incoming passengers from Europe and more nations are likely to follow suit. As per the latest assessment by International Air Travel Association (IATA), there may be a passenger revenue loss ranging from $63 billion to $113 billion which is almost 11%-19% of global passenger revenues, based on the current spread of the virus. This will not only lead to sharp declines in airline revenues but also raises the prospect of large losses in most of the larger airlines specifically in the current and next quarter. Many of them have already resorted to capacity back downs through route withdrawals and may even opt for rationalization of the work force in the near term to ensure the sustainability of their operations.

The spill-over effect of the Covid-19 crisis on the Indian aviation sector is likely to be very significant over the March-May period. While the reported number of infections in India stand as of now at 80 and deaths have been limited (only two so far), the central government and the state governments have already initiated drastic measures to stem the expected spread of the virus. These measures include the temporary suspension of foreign visas up to April 15, 2020 (except a few categories) by the central government and embargo on public events, shutdown of schools, malls and other places of public activity by an increasing number of state governments. All these measures and along with it, the increased risk of contagion in public spaces have led to an increasing impact on airlines through ticket cancellations and a rapid slowdown in fresh bookings.

With large scale cancellation of business conferences and events, the impact on business travel is likely to be severe in the near term. Further, the virus threat has emerged just before the start of the holiday season in India in April. A study undertaken by Acuité Ratings indicates that historically, the growth in domestic passenger traffic has been high at 16%-23% during the 3 month period March-May except in 2019 when the cessation of operations of a large domestic airline i.e. Jet Airways had an effect on passenger throughput (please refer to Graph 1). We, however, expect a significant negative growth in monthly domestic airline traffic which can go as high as 50% at least up to June 2020, depending on the severity of the outbreak in India in the near term. The latest data from DGCA shows a modest growth of 2.2% in January 2020 when it only reflected the general slowdown in the economic environment and had not yet seen any effect of Covid-19.

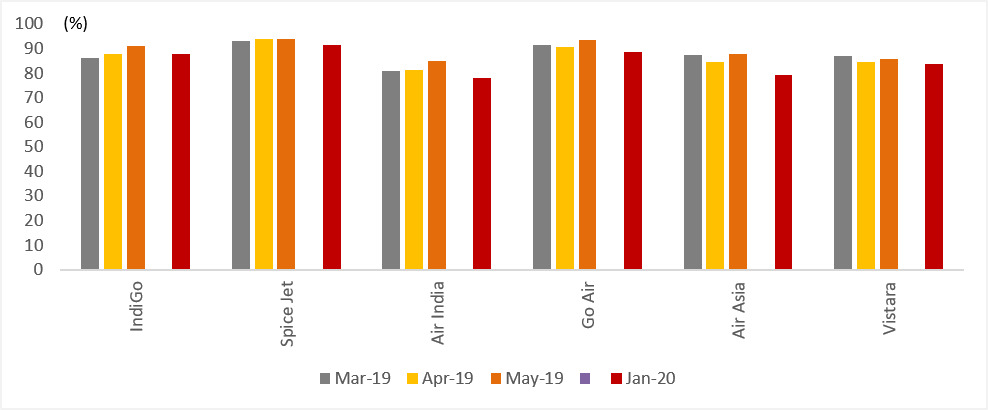

Further, the passenger load factor (PLFs) for almost all the airlines had been high with an average over 85% during the period of March-May 2019, the peak domestic tourist season (Graph 2). Among the carriers, Spice Jet had registered the highest PLF of 93.5% followed by Go Air (91.8%) and IndiGo (88.2%). Clearly, the drop in passenger volume will also have a sharp impact on the average PLF during this period and a dip to 50%-60% over the next 3 months is not an unlikely scenario.

The average peak season fares have consistently declined over the past few years amid high competition although it has stabilised to some extent last year due to the cutback in sector capacity brought about by the exit of Jet Airways. Normally, the month of April marks the beginning of the vacation season in the country and a spurt in family leisure travel, thereby encouraging airlines to raise fares. Clearly, this year is different with airfares set to decline substantially over the next 2-3 months, given the rapidly rising levels of cancellations in personal travel planned for the summer months along with the severe downturn in business travel triggered by the travel advisories issued by both the government and individual companies.

The risk of a sharp fall in fares is borne out by the fact that flight tickets in the trunk route between Delhi and Mumbai over March 22- March 28, 2020 are already available for around Rs. 3700, down from an average of Rs.4200 witnessed during February 2020; similar trend can be seen over the other key routes of Bangalore-Delhi and Bangalore-Mumbai where fares have dropped over the past two weeks. The reduction in fares along with the sharply lower passenger load factors, are thus expected to lead to a precipitious drop in the operating margins of the airline companies in Q4FY20 and Q1FY21. The airlines who have a higher presence in international routes clearly will witness a sharper impact. The operating margins (earnings before interest, depreciation, amortisation, tax and rentals, EBITDAR) of the listed airline companies i.e. Interglobe Aviation (Indigo) and Spice Jet typically has ranged between 18%-30% over the last few quarters depending upon the seasonal factors; in a likely scenario that the quarterly EBITDAR margins drop below 10%, substantial losses may be incurred particularly in the case of Spice Jet which has already seen higher costs due to the continued grounding of its 737 Max aircrafts. However, we also expect that with increased cancellations and poor bookings, most of the airlines will take corrective steps such as temporary cessation of flights in certain routes which will not only reduce costs but also arrest any persistent decline in airfares. Additionally, the severe margin pressures will get offset to an extent by the drop in ATF prices brought about by the fall in global crude prices.

.png)

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD