Given the mixed signals originating from both domestic as well as international vantage points, the MPC is unsure of which direction to take – atleast in the short term. Further data is therefore awaited pertaining to inflation (influenced by agricultural output) and whether consumption and investment comes back on line. The decision on interest rates is consequently in a state of flux as there seems to be no clarity as to how the economy will react to further monetary loosening.

The Monetary Policy Committee (MPC) has refrained from cutting interest rates and has maintained the status quo. The committee appeared to be concerned about the evolving growth-inflation dynamic, given the rising inflationary tendencies during a slowdown. Due cognizance was given to the household inflationary expectations, capacity utilization levels along with kharif output. Based on these parameters, in its assessment, the committee was with the view that inflation tendencies are realistic in the short to medium term – nevertheless reverting to the mean by Q2 FY21.

In its previous assessment, while the MPC had pegged the Q2 CPI number to hover near the 3.4% level, for H2 FY20, the range was estimated to be 3.5-3.7%. Given the fact that the actual inflation averages were within those ranges, the committee is confident that its inflation outlook remains consistent with realty. Despite this, there remains certain concerns regarding food inflation, which has infact approached the 7% level, a 3 year high. Spikes in vegetable prices (especially onions) along with minor pressures seen in traditionally deflating commodities such as pulses, milk and to an extent meat have caused significant uncertainty among planners.

In the light of these propensities, the committee was concerned with the fact that core inflation (excluding fuel and fuel) has been moving in the opposite direction. The metric actually came down by 80 bps since September, recording 3.4% in October, while food inflation was rising by almost that quantum. A falling core inflation is a matter of worry during a slowdown because it points towards falling demand for consumer durables & non-durables. This in turn has a negative implication for capital goods as well because the demand for such items is a function of capacity augmentation and capex. Since the rate of change in investments (Gross Fixed Capital Formation) is alarmingly low, especially apparent post the Q2 revelations, falling consumer demand can mean a lot of things; Stagflation could be one of explanation.

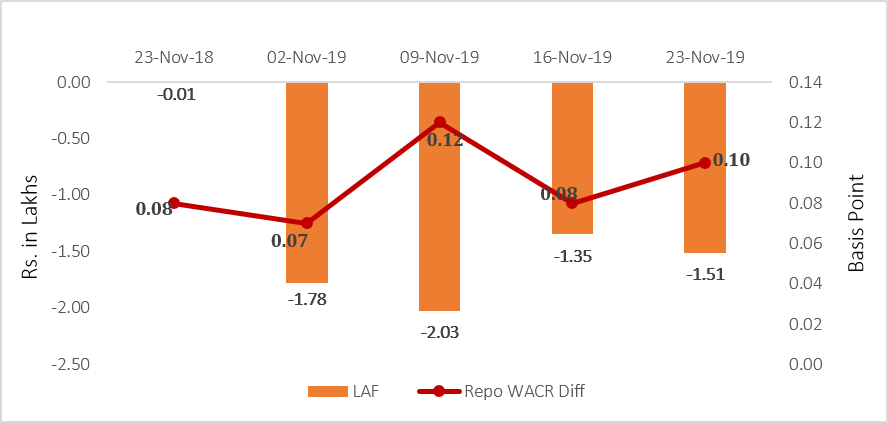

On the topic of liquidity management, the MPC deliberated on the systemic conditions and LAF operations. It was assessed that daily absorptions (under Reverse Repo operations), amounted to the tune of almost Rs. 1.9 lac crores. In addition, given Government of India’s availing the Ways and Means Advances (WMA) facility, an incremental absorption of Rs. 0.8 lac crore was initiated (under Longer Term Variable Rate Reverse Repo operations). The WMAs are short term credit facility made available by the RBI to the Government (both Centre and State) for a period not exceeding 3 months for meeting short term liquidity mismatches in return of G-Secs as pledges. The incremental absorptions in this case helped the Government raise money in order to meet its fiscal obligations while pushing Government securities to ever eager commercial banks. Nevertheless, the condition points to the fact that liquidity conditions are healthy and WACR movement nearing the Reverse Repo rate (4.9%) is a clear indicator.

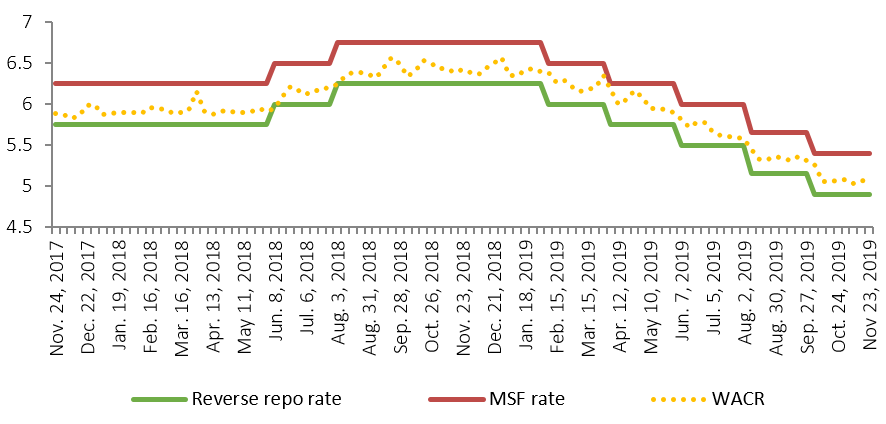

Acuité policy corridor, which is a Bollinger band consisting of the MSF (upper bound) and Reverse Repo (Lower bound) suggests that there exists sufficient liquidity in the system. Therefore, theoretically speaking there was no need for a rate cut at this time. However, the decision to cut rates, if taken would have been primarily influenced by the need to communicate the RBI’s accommodative stance in order to boost the sagging market sentiment.

Taking cues from the global circumstances, the MPC’s decision to hold rates wasn’t influenced by the recovery of sorts in the US, EU and Japan. This is because much of these recoveries were moderated by insecurities pertaining to US-China trade war, poor consumer sentiment in much of these markets. Meanwhile, low commodity prices in turn stymied the fiscal expansion powered progress of commodity exporter economies. Given these mixed signals emanating from both domestic as well as international vantage points, the MPC is unsure of which direction to take – atleast in the short term. Further data is therefore awaited pertaining to inflation (influenced by agricultural output) and whether consumption and investment comes back on line. The decision on interest rates is consequently in a state of flux as there seems to be no clarity as to how the economy will react to further monetary loosening.

Liquidity Operation by

RBI:

Source: RBI, Acuité Research;

Note: Net injection (+) and Net absorption (-)

Policy Corridor and WACR:

Source:

Acuité Research

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD