KEY TAKEAWAYS

India’s IIP growth decelerated sharply to 3.1% YoY in Sep-21 from 12.0% (revised upward from preliminary estimate of 11.9%) in Aug-21. While market participants were expecting industrial activity to moderate due to fading favorable statistical base, the actual annualized IIP print turned out to be weaker than consensus expectation of around 4.8% YoY. Moreover, it was also accompanied by a 2.6% MoM contraction in sequential activity - the first sizeable contraction in sequential industrial production post the second wave of Covid in Apr-May 2021, reflecting some slowdown in industrial recovery.

Key Takeaways

Outlook

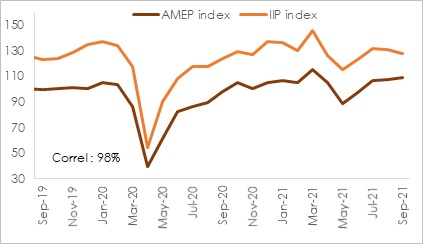

In our previous month’s coverage on IIP, we had highlighted the likelihood of annualized IIP growth drifting lower into single digits amidst fading of favorable statistical base effect. The Sep-21 print has reinforced that expectation while also highlighting the impact of few temporary disruptions like adverse weather conditions and the global energy crisis. The overall trajectory of IIP is very well reflected in our proprietary AMEP index (Acuité Macroeconomic Performance Index), which after having recovered post the disruption caused by the second Covid wave, is showing signs of plateauing. (Chart 2)

Going forward, to correctly interpret growth scenario, it will be critical to look at sequential momentum, which we expect to remain supportive amidst:

Progress on vaccination: At present, India has inoculated around 54% of its population with single dose and fully vaccinated around 26%. As coverage nears 2/3rd of the population by year-end, it should provide a strong boost to consumer sentiment and demand recovery.

On the downside, we continue to be mindful of risks from global supply chain disruptions along with elevated commodity prices that can dampen demand and potential financial market volatility as key central banks begin to normalize their monetary policy. Another wave of Covid cannot be ruled out, though the economic impact could be much lower on account of vaccine penetration and existing seroprevalence.

As such, we continue to retain our FY22 growth forecast at 10.0% with downside risks.

Annexure

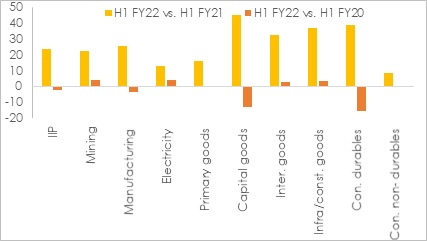

Chart 1: IIP for H1 FY22 still at -2.2% lower vs. pre-pandemic level

Chart 2: AMEP index serves as a predecessor to IIP index

Table 1: IIP Growth at a glance

|

Weight |

Sep-20 |

Sep-21 |

Apr-Sep |

Apr-Sep |

|||

|

IIP |

100.0 |

1.0 |

3.1 |

-20.8 |

23.5 |

||

| Sectoral Classification | |||||||

|

Mining |

14.4 |

1.4 |

8.6 |

-15.2 |

22.3 |

||

|

Manufacturing |

77.6 |

0.4 |

2.7 |

-23.3 |

25.3 |

||

|

Electricity |

8.0 |

4.9 |

0.9 |

-8.0 |

12.8 |

||

| Use-Based Classification | |||||||

|

Primary Goods |

34.1 |

-1.5 |

4.6 |

-14.2 |

15.8 |

||

|

Capital Goods |

8.2 |

-1.2 |

1.3 |

-40.2 |

44.9 |

||

|

Intermediate Goods |

17.2 |

-0.4 |

4.9 |

-22.8 |

32.4 |

||

|

Infrastructure/Construction Goods |

12.3 |

4.0 |

7.4 |

-24.8 |

36.9 |

||

|

Consumer Durables |

12.8 |

5.3 |

-2.0 |

-39.0 |

38.4 |

||

|

Consumer Non-Durables |

15.3 |

2.4 |

-0.5 |

-8.2 |

8.3 |

||

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD