In India travel & tourism industry continues to be one of the fastest growing sectors. Not only it contributes significantly to the country's GDP but is also an important source of employment generation. Further, it acts as a source of earning foreign exchange for the country. Consequently, the booming tourism industry has had a cascading effect on the hospitality sector with an associated rise in the occupancy rates (OR) and average room rates (ARR) across the major cities in the country.

According to World Travel & Tourism Council (WTTC) ranking, India ranks third after China and the US underpinning the country’s position in the travel and tourism industry.

Since the hotel industry primarily depends on the growth in travel and tourism, any subsequent rise in the industry translates a positive for the hospitality industry. Over the past few years, with steady increase in tourists both domestic and foreign, the country has witnessed an emergence of hotels to cater to the required demand.

During FY19, the country received 10.6 million foreign tourists as compared to 10.4 million in the previous year. In fact, forex earnings from tourism stood at $27.7 billion in FY19.

The overall average occupancy rates (OR) rose to ~67% in FY19 in 11 major cities of India from ~66% in FY18 on the back of increased demand from domestic and foreign travellers for business and leisure activities. In fact, the OR for five-star deluxe hotels too was recorded at ~67% in FY19 following the growing trend. On the other hand, the overall average room rates (ARR) increased by about 3% to Rs 5,900/day in FY19 (11 major cities of India) from Rs 5,700/day in FY18 as per the available industry information. While the five-star deluxe hotels achieved an ARR of ~Rs 10,600/day growing by ~4% from Rs 10,300/day in the previous year.

Further, the industry is expected to be driven by increase in disposable income, growing desire for travel and tourism across age groups, and opening up of new travel destinations. Also, the government's focus on improving the country's tourism industry bodes well going ahead.

Over the past few years, with steady increase in tourists both domestic and foreign, the country has witnessed an emergence of hotels to cater to the required demand. The hotel industry thus, which can be classified as business and leisure destination is one of the prominent industry.

During FY19, the country received 10.6 million foreign tourists as compared to 10.4 million in the previous year. As the hotel industry is primarily dependent on the growth in travel and tourism, any subsequent rise in the industry translates a positive for the hospitality industry.

The overall average occupancy rates (OR) rose to ~67% in FY19 in 11 major cities of India from ~66% in FY18 on the back of increased demand from domestic and foreign travelers for business and leisure activities. In fact, the OR for five-star deluxe hotels too was recorded at ~67% in FY19 following the growing trend. Major cities such as Mumbai, New Delhi, Goa, Kolkata and Hyderabad witnessed higher OR’s than the overall average signifying higher demand in these regions which are characterized by corporates, government offices, diplomatic missions and leisure destinations.

On the other hand, the overall average room rates (ARR) increased by about 3% to Rs 5,900/day in FY19 (11 major cities of India) from Rs 5,700/day in FY18 as per the available industry information. While the five-star deluxe hotels achieved an ARR of ~Rs 10,600/day growing by ~4% from Rs 10,300/day in the previous year. The overall average ARR was led by Mumbai, Goa, followed by New Delhi at an all India level.

The proposed inventory as per the available information publicly is expected to come up majorly in Mumbai (comprising majorly upper mid-market and luxury), Bangalore (upscale market), Jaipur (upscale market) and Goa (upscale market).

Despite, the mid-market and upper mid-market segments continuing to attract higher interest of hotel investors and developers over the past few years, the share of the upscale-luxury segment is lately witnessing an uptick. In fact, the expected new supply entering this space is likely to rise owing to increase in disposable income, growing desire for travel and tourism across age groups, and new travel destinations.

Acuité believes the industry is likely to witness growth owing to increasing demand underpinned by rise in travel and tourism space coupled with higher spending capacity across domestic age groups.

The competitive dynamics witnessed by the industry players remain contingent to the location and level of service they provide. In fact, competition remains high in metros owing to the higher supply and players offering similar services. Further, with rising penetration of foreign hotel chains the competitive scenario has further risen.

The location based competition is faced by players operating in places such as Goa, Agra and Jaipur, accounting competitiveness in the branded segment. Consequently, the room rates remain under pressure albeit Goa and Jaipur have continued to hold on to their market by commanding a premium. However, business destinations remain exposed to this vagaries.

Moreover, the loyalty programs too, drives a customer’s decision. Notwithstanding, the prices to an extent remain a differencing factor but the quality of service is paramount. Hence, despite increase in the competitive intensity, well established brands catering the market have been able to charge the premium rates over competition.

Further, emerging trends such as online hotel bookings has become a major revenue contributor and emerged as a prospective opportunity to players.

Acuité believes the competitive intensity remains high in the premium segment with the rising penetration of foreign players dampening players market retain ship.

While the room revenues are a direct function of room rates and occupancy rates, in terms of the cost structure for the hotel industry as a whole, employee costs are one of the largest cost components accounting for about 25-30% of the total expenditure. Whereas selling & distribution costs account for about 15-20% of the operating costs which includes advertising expenses and marketing costs followed by power & fuel which make up for 8-10%.

Further, the F&B consumes about 10-15% of the costs on an average. Other operating costs account for the remaining costs which include the repairs and maintenance, travelling expenses, etc. among others.

Availability of skilled workforce is critical to the industry and requires to grow proportionately with the sector. The shortage is caused owing to absence of organized training and educational institutes for development of skilled employees coupled with high attrition levels.

Acuité believes the industry’s exposure to input related risk remains within manageable levels.

Notwithstanding, the government's focus on improving the country's tourism industry which bodes well, the sector also faces several challenges on account of complex regulatory scenario. The industry faces regulatory constraint in the process of development starting from land acquisition stage. Multiple windows of clearances, leads to tedious and a time-consuming process.

The government introduced GST in July 2017 with the aim of replacing the indirect taxes on all goods and services. Initially, there was a higher tax rate of 28% (for room tariffs of Rs 7,500 and above), however, this has been revised and rationalized to 18% which augurs well for the sector and can boost tourism. Further, those between Rs 1,000 and Rs 7,500 is set at 12%.

Moreover, during March 2017, the Supreme Court had ordered a ban on sale of liquor by establishments which included premium hotels, falling within the 500 meter radius of state and national highways which had adversely impacted the revenues of the industry albeit for short period.

Acuité believes the industry is likely to witness buoyancy owing to underlying government support both at the state and central level.

With the emerging trends related to online booking platforms for hotels, it is imperative for the players to adopt the transition. The industry players need to continue investing in the latest upgrades rendering high level of services to its guests. However, these risks are not significant to the industry as major hoteliers are cognizant to this fact and have already undertaken prudent measures.

Acuité believes that the industry is less exposed to technological risks and is likely to be at a favorable level going ahead.

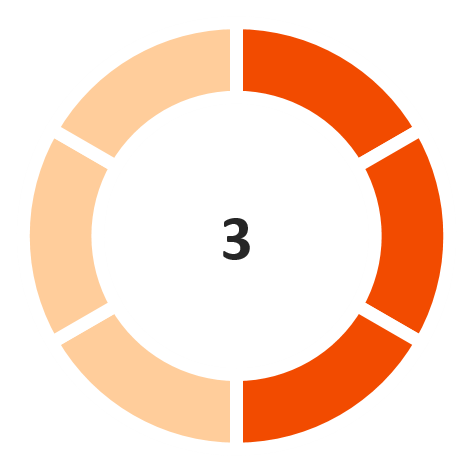

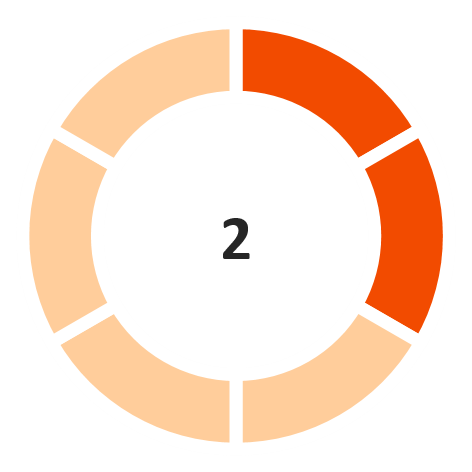

Operating Margin

(Marginally favorable)

Interest Coverage Ratio

(Marginally unfavorable)

Return on capital employed

(Unfavorable)

Debt/ Equity

(Marginally favorable)

GCA days

(Favorable)

Note: The industry financial performance risk score is provided on a 6-point scale

Disclaimer:

Acuité IRS should not be treated as a recommendation or opinion that is intended to substitute for a financial adviser's or investor's independent assessment of whether to buy, sell or hold any security of any entity forming part of the industry.

Acuité IRS is based on the publicly available data and information and obtained from sources we consider reliable. Although reasonable care has been taken to ensure that the data and information is true,

Acuité, in particular, makes no representation or warranty, expressed or implied with respect to the adequacy, accuracy or completeness of the information relied upon.

Acuité is not responsible for any errors or omissions and especially states that it has no financial liability whatsoever for any direct, indirect or consequential loss of any kind arising from the use of Acuité IRS.

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD