India was the third largest producer of electricity in the world in 2018. Moreover, the country is witnessing a sustained rise in the per capita consumption of electricity over the past few years. However, it still lags behind its BRICS counterparts which have a higher per capita consumption. As on October 2019, the overall installed power capacity of the country was at ~364 GW.

During FY19, installed capacity from thermal sources made up ~64 percent of the overall capacity and accounted for about 78 percent of the overall generation in India. However, with the country’s inclination more towards renewable energy coupled with the sustained stress in the private power gencos, investment in new coal-fired power plants is expected to be limited, in at least the next five years. However, going ahead with gradual pick up in power demand and retirement of old and inefficient units, investment in coal based capacity is expected. Further, with the government’s ambitious targets primarily in the renewable energy capacity addition, it would require huge investments in the country’s distribution sector which is the final segment in the value chain and will remain a key monitorable. Moreover, with the government’s initiative such as providing 24x7 power to all consumers, giving last mile connectivity under SAUBHAYA scheme will further require efficient distribution network.

Historically however, the power distribution companies (discoms) have always been the weakest link in the entire power sector value chain despite being the most critical and being the interface with the final consumer. Plagued with huge outstanding debt leading to high interest outgo, losses incurred on account of disproportionate cost recovery and surging aggregate technical and commercial (AT&C) losses have over the years crippled the sector. Following which the government launched the UDAY scheme to revive the sector under which the discoms were required to improve their financial and operational efficiencies. The scheme envisaged to reduce interest burden, cost of power and AT&C losses which ultimately would lead to adequate and reliable power enabling 24x7 power supply.

However, the discoms have not been able to meet some of the key targets laid under the scheme. AT&C losses which were supposed to be under 15 percent by FY19 continue to trend upward. ACS-ARR gap which needed to be eliminated by the said fiscal continues to persist. Inadequate tariff revisions and lower operational efficiencies have continued to be the hindrances in target achievements.

Key risks & attributes

In FY19, base power deficit (difference between the demand and supply of electricity) was recorded at 0.6 per cent, whereas peak deficit was at 0.8 per cent. In fact, during H1FY20 base deficit was at 0.5 percent and peak deficit was recorded at 0.7 percent. Power deficit continues to be relevant in the country primarily because of discoms reluctance to buy power, owing to financial stress which they are under leading them to resort to load shedding. Discoms which have been reeling under heavy losses due to under-recovery of costs leading to rising ACS-ARR gap have led them in becoming financially unviable. High AT&C losses, delayed subsidy payments from respective states and high cross subsidization is also hampering their feasibility. Moreover, owing to tepid power demand growth, it further contributes to the financial woes of discoms. Further, in cost- plus power purchase agreements discoms have to bear fixed cost charges even if there is back down in power demand. Backing down also leads in having a cascading impact on the generation sector particularly on the private players who too are under stress due to lower utilization of plants.

Despite the government’s several initiatives over the years such as rural electrification, power to all and most recently the SAUBHAYA scheme, demand hasn’t picked up as expected and recorded a tepid five percent y-o-y growth in FY19. Notwithstanding, going ahead with rising economic growth and ease of power accessibility demand is likely to pick up. Moreover, the key challenge for the government would be demand estimation for effective forecasting, scheduling and subsequent policy implementation.

Acuité believes that the state discoms need to undertake timely tariff revisions in order to become financially viable. Further, operational efficiency in terms of reduced AT&C losses, too, need to be addressed.

Broadly, competition is low in the sector with state-owned utilities namely the state discoms largely dominating the sector. Only a few private players are currently present in the sector owing to the highly regulated business model. Lately, however private sector players which have shown improved operational efficiency has led to the government’s intent of having more private sector participation in the sector to improve competitiveness. In fact, the government has proposed through an amendment in the electricity act to segregate the carriage from content in the distribution sector. It is planned to introduce multiple supply licensees in the content, based on market principles, and continue with the carriage as a regulated activity.

New models such as the distribution franchisee too have been operational in states such as Maharashtra, Odisha, Uttar Pradesh and Rajasthan by private players such as Torrent Power, CESC. Implementation of the franchise model is expected to help the discoms become efficient in terms of billing and collection of electricity dues. Under the model, an area is tendered out to the highest bidder by the particular state discom who manages billing and collection on behalf of the discom. Another model which is likely to attract traction going ahead is the public private partnership (PPP), which is currently witnessed in Delhi.

Acuité believes competition risk in the sector to be low in the short term. However, in long term with state discoms inability to show any significant improvement, entry barriers are expected to be lowered with policy initiatives such as separation of carriage and content. Public-Private Partnership (PPP) model is also likely to bring in competition.

High power purchase cost is the primary input related risk for the power distribution sector. The said cost forms more than half of the entire expense borne by a discom. Historically, the actual cost of supply incurred by the discoms has always exceeded the average revenue required leading to the mismatch in realised revenue and thus causing the rising ACS- ARR gap. The major component of the cost of supply pertains to the power procurement costs (PPC) from the gencos. With India being mostly a coal dominated power generating country, the PPC is majorly related to variation in the energy charges as the fixed charges are mostly stable (for capacities on cost-plus basis). Over the past few year’s production of coal has however witnessed sustained growth. Further, with the government’s initiative of higher coal production and increased allocation to the power sector, availability of coal stocks to remain healthy going ahead. Moreover, bottlenecks related to coal transportation too are being addressed through investments in rail connectivity by laying new lines and increase in the rake availability for the power sector. Consequently, energy charges to remain fairly stable for capacities based on domestic coal. However, capacities based on imported coal remain exposed to geographical risks such as extreme weather conditions in the importing country affecting production, demand- supply situation and policy changes in the respective producing countries.

Acuité views input related risk to be unfavorable with coal availability to remain a critical parameter for the sector, leading to the variation in the PPC costs and subsequently the cost of supply.

The power sector is highly regulated by the government primarily by the electricity regulatory commissions (ERC’s) most notably the CERC and SERC’s. While the CERC apart from regulating the tariff for central gencos, regulates the tariff of gencos and transcos functioning at the inter-state level it also plays a vital role at a broad level in policy making by undertaking the role of providing advisory functions and being the adjudicator in resolution of disputes. On the other hand, the state commissions play a very important role at the intra-state level with respect to tariff regulation and determination. It regulates electricity purchase and procurement process of respective state discoms (including the price) through agreements for purchase of power for distribution and supply within the state. It further lays down the criteria for ensuring proportionate cost coverage for the discoms provided it meets certain performance standards.

Some of the other key functions of the state commissions include issuing licences for the purpose of power transmission, distribution and electricity trading within the state, determining the tariff for generation, supply, transmission and wheeling of electricity within the state, facilitating intra-state transmission and wheeling of electricity.

Thus, the key risks emanate from the fact that the respective state ERC’s which are entrusted with aforesaid functions might enforce some regulatory changes or even some more stringent performance criteria for the discoms thereby even forbidding the coverage of certain cost components leading to disproportionate cost recovery and consequently the financial stress in the discom books.

Acuité views regulatory risk in the distribution sector to be unfavorable. Being one of the most critical sectors from the political viewpoint any drastic policy changes or deregulation in the sector is highly unlikely at least in medium term. Further, looking at the current precarious position the state discoms are into financially, efficient cost pass through mechanisms for the discoms need to be addressed by the commission.

Having a poor electrical infrastructure is the biggest challenge in having a reliable and quality supply. Problems like ageing transmission and distribution infrastructure, huge AT&C losses and unavailability of power supply infrastructure in economically unviable places namely locations of geographically harsh terrains possess a challenge. The north-eastern part of the country is quite evident for facing such hurdles and thus has not been able to have reliable power supply.

Annually the country losses a significant quantum of power due to power theft, which is one of the highest in the world. Types of electrical power theft, include tapping a line or bypassing the energy meter etc. Therefore, use of new age technology such as smart metering is also being undertaken by the government to eliminate the same. Further, Integrated Power Development Scheme (IPDS) was launched with the objectives of reduction in AT&C losses, establishment of IT enabled energy accounting/auditing system, improvement in billed energy based on metered consumption and improvement in collection efficiency.

Acuité views technology upgradation in the distribution sector to improve efficiency gains of discoms. Dynamic power demand forecasting tools, smart metering or GPS tracked boxes in the electricity feeder could help monitor meter tampering, power theft and non-payment of electricity bills, thereby aiding AT&C losses reduction.

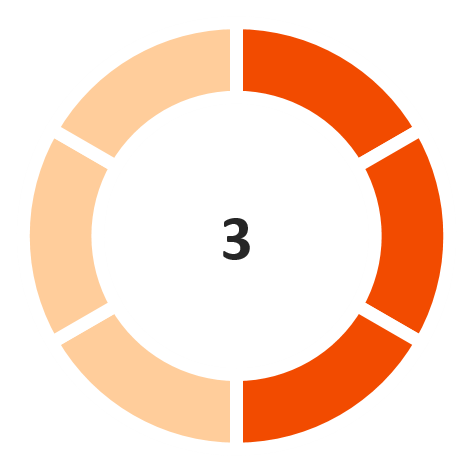

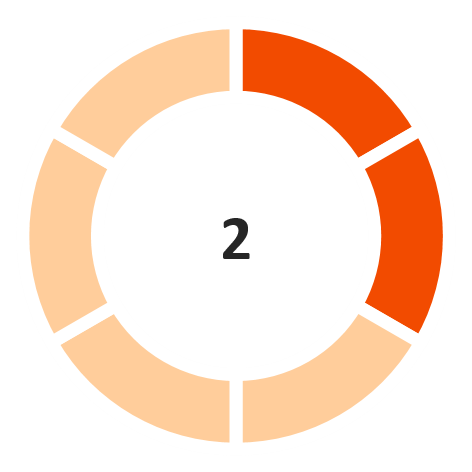

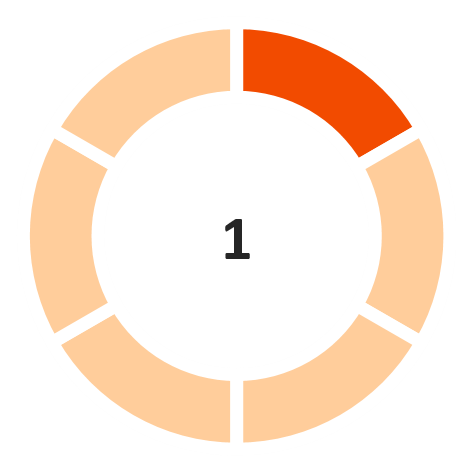

Operating Margin

(Marginally unfavorable)

Interest Coverage Ratio

(Unfavorable)

Return on capital employed

(Highly unfavorable)

Debt/ Equity

(Unfavorable)

GCA days

(Marginally unfavorable)

Note: The industry financial performance risk score is provided on a 6-point scale

Disclaimer:

Acuité IRS should not be treated as a recommendation or opinion that is intended to substitute for a financial adviser's or investor's independent assessment of whether to buy, sell or hold any security of any entity forming part of the industry.

Acuité IRS is based on the publicly available data and information and obtained from sources we consider reliable. Although reasonable care has been taken to ensure that the data and information is true,

Acuité, in particular, makes no representation or warranty, expressed or implied with respect to the adequacy, accuracy or completeness of the information relied upon.

Acuité is not responsible for any errors or omissions and especially states that it has no financial liability whatsoever for any direct, indirect or consequential loss of any kind arising from the use of Acuité IRS.

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD