Brief: Based on forward rate calculations, the current consensus holds that yields will come down further and may open a window for issuers.

Impact: Positive (Bond Market)

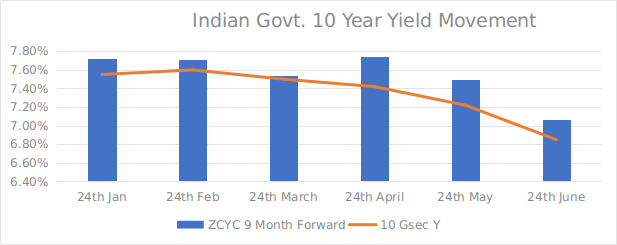

The Indian 10-year Government Security (GSec) yields have been volatile lately given the undershooting inflation figures in the domestic market along with confusing signals emanating from the US Federal Open Market Committee (FOMC) and the European Central Bank (ECB). Nevertheless, the yields on the said instrument has come down from the peak of 7.55% as on 24th January 2019 to 6.85% as on 24th June 2019. These declines are also helped by the two back to back cuts in the Repo rate, which now stands at 5.75%.

What this means for the yield curve is the fact that the difference between an ultra-short duration money market instrument yield and a 10-year government security yield seems to be more realistic, currently hovering near the 110 bps. Flashback mid-2018, this differential was nearly 200 bps – almost double to what it is today.

Given the benign situation on the inflation front and the concerns pertaining to the macroeconomic slow -down, the MPC is under enormous pressure to cut rates further. Even considering the short-term scenario, where the consumer price index is expected to breach the 3% target (H2 FY20), thanks to food inflation, the pressure to accommodate will most likely persist. Therefore, the current consensus holds that yields will come down further and may open a window for issuers.

Based on the zero-coupon yield curve, a 9 year forward rate of a 10-year zero coupon instrument held for 1 year was calculated. The exercise revealed that the market is expecting yield of 7.07% as on June 24th 2019. Adjusting for coupon paying 10-year GSecs, the effective yield comes to 6.85%. Assuming further rate cuts and no external pressures emanating from the US Fed, this may comfortably reach the 6.55% level by end September 2019. For reference, 9-year forwards have declined from 7.72% in January to 7.07% in June this year.

In another approach, we forecasted the 10-year GSec yield through a vector error correction model (VECM) using Indian Repo rate and 10-year US GSec yield as independent variables. Here too, the results show that the Indian yields may fall to 6.35% (lower bound) in the considered time frame. The two results lead us to believe that substantial yield declines can be foreseen over the next quarter.

The situation is likely to prevail if the status quo persists. However, in case of middle east tensions unrealistically inflating commodity prices and China managing to receive a full waiver from the US, the hypothesis may not hold.

Source: Acuité Research

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD