RBI’s systemic liquidity

management has been mostly effective. For the most part, the WACR/ Repo differential

has been at parity, signifying the central bank’s neutral stance. However,

recent fluctuations are noticeable especially since September 2018 (Q2 FY19).

The said time frame was characterized by a high interest rate environment from

both the domestic and international perspective. Consequently, the capital

market was impacted significantly and all financing activities were shifted to

the traditional sector. Even though, in the initial phase, a lot of burden was

taken over by the NBFC space, asset liability mismatch pressure took the source

out of action. Commercial banks therefore emerged as the primary financiers of

the economy’s capital requirement and off-take levels crossed the 14% threshold

in the period.

Given the fact that a significant portion of public banks found themselves under restrictive lending (as per PCA obligations) as well, the systemic stress on the remaining institutions increased substantially. Demand for credit however continued to grow and out-competed the growth in deposits by almost 500 bps. A situation that resulted in the credit to deposit ratio stretching beyond the comfortable 75% level and relentlessly approaching 80%, a historic high.

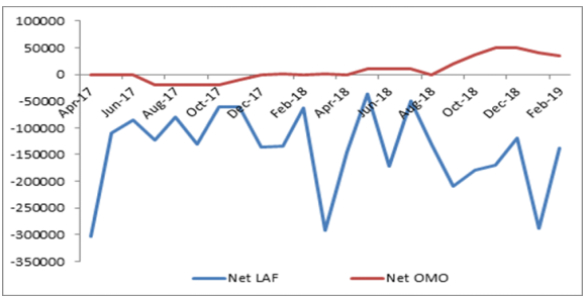

While activity under LAF was not significantly different and remained consistent with previous estimates, a change in other liquidity avenues was apparent. Activity under OMOs is a special mention here. Before the said period, average monthly net infusion was Rs. 6,100 core. Post the liquidity crunch, this infusion increased to Rs. 42,000 crore on average. The after effect of this massive infusion was the exhaustion of collaterals as HQLA (non SLR) assets declined over time. Since SLR and CRR requirements remain intact, banks no longer have enough collaterals to trade for cash in the open market or any RBI sponsored window.

With the LAF and OMO avenues unable to offer comfort to the system, the RBI has opened up a third avenue in the form of Currency Swap (3 years forward). Under this arrangement, the RBI will form a counter party arrangement with commercial banks. The buy-sell contract will allow RBI to buy USD from premium paying counter parties and in return provide INR. At this time, the currency swap arrangement is worth $5 billion, which approximately translates to Rs. 34,500 crore (prevailing exchange rate). This quantum, we reckon can sustain the systemic deficit for three months (in conjunction with other avenue).

We calculate the systemic deficit by considering monthly incremental credit and deposits. We have noticed a significant variance in both these accounts post the September 2018 period. While incremental credit has increased from Rs. 48,000 crore to Rs. 56,000 crore (monthly average) in the time frame, incremental deposits on the other hand declined from Rs. 54,000 crore to Rs. 42,000 crore (monthly average). The resultant monthly incremental deposit-credit spread has therefore widened from Rs. (+) 6,000 crore to (-) Rs. 14,000 crore in a matter of a few months.

To compensate for the adverse

credit to deposit ratio, there have been hectic OMO activity, seeing an

incremental ~Rs. 36,000 crore infusion (monthly average). As pointed out

earlier, this has caused a severe shortage in available collaterals with

commercial banks, resulting in the so called – ‘collateral constraint’

situation as apparent from the uncomfortable declines in the HQLA (less SLR)

metric. Given these conditions, we estimate that the Swap deal will allow RBI

to infuse roughly three-months’ worth of liquidity shortfall – amounting to Rs.

11,667 crore (monthly average). This brings us to the understanding that this

is not a one-off solution and this space will see continued activity in the

coming quarters as banks scramble for liquidity in a fast expanding economy. In

Swaps therefore, RBI has found itself a third avenue of monetary management.

Despite the initial inactivity/ scant volatility, how this impacts the currency

as well as money/ capital markets, remains to be seen.

Net Debt Issuance by Centre and State Government:

Source: Acuité Research, RBI

Source: Acuité Research, RBI

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD