Impact: Positive (Commercial Bank Financial Performance)

Brief: Our analysis reveals that larger banks are safer and more efficient as compared to those with smaller asset size. In terms of better management of non-performing loans (NPAs), Net Interest Income (NII) and Return on Assets (ROA), banks with comparatively larger asset size perform better.

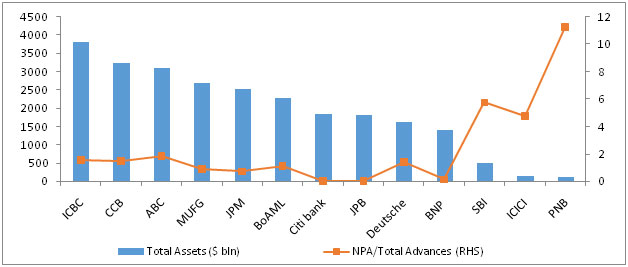

We analyzed 13 of the world’s largest commercial banks and compared their key financial metrics to reach a conclusion. As per the methodology, global commercial banks were stacked up based on their asset size and then variables such as Non-Performing Loans/ Advances (NPA), Return on Asset (ROA), Net Interest Income (NII), Return on Equity (ROE) and Capital Adequacy Ratio (CAR) were compared.

As per our assessment, a larger asset size translates into better financial performance for commercial banks. The analysis reveals that with every $100 billion increase in asset size, Non-Performing Loans (NPA) reduce by 15 bps. The variables, asset size (independent variable) and NPA (dependent variable) were negatively correlated and found to be statistically significant. In terms of Net Interest Income (NII), for every $1000 billion increase in asset size, NII improves by 20 bps. Even a bank’s Return on Assets (ROA) metric returned a surprising correlation with asset size; for every $100 billion increase in assets, there is an improvement of 40 bps in ROA.

While comparing CAR and NPA, we found that for every 1% increase in the former, the latter reduces by 66 bps. A higher CAR is a function of an optimized Tier 1 (CET1), Additional Tier 1 capital and lower Risk Weighted Asset (RWA) ratio and we see asset size positively impacting this number. In our sample size, the three largest commercial banks recorded a CAR of 15.1% as compared to 13.5% among the three smallest. Also, in terms of effectively managing resources, the three largest commercial banks recorded an ROA of 1.07 as compared to (-) 0.30 for the bottom three.

Even for profitability, size does matter. The Net Interest Income (NII) for three largest commercial banks (by asset size) averaged almost $70 billion as compared to just $5.4 billion for the bottom three. Coming to the Non-Performing Advances/ Loans management, the picture becomes much more clear. The top three banks have an average NPA of just 1.6% as compared to 7.3% for the bottom three. Despite being preliminary, what this regression analysis suggests is that commercial banks with large asset sizes are better able to manage their finances and are thus more efficient.

Source: Commercial Bank Annual Reports

Source: Commercial Bank Annual Reports

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD