Impact: Negative (Agro Based Industries)

Brief: Higher MSP may not tangibly improve agro-industry performance and realizable price for cultivators

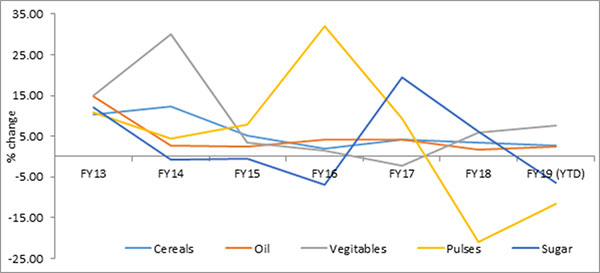

Among the agro commodities, price of pulses is one of the most volatile in India. It is observed that the average inflation rate for the commodity was 33% for nearly 15 months between June, 2015 to August 2016. We have therefore identified the commodity as representative in our study on impact of MSP.

As per our analysis, pulses inflation is highly correlated with MSP (Minimum Support Price) (-0.41) and production (-0.81) of the previous year. An inverse correlation of inflation rate with production is understood as agro commodities follow hog cycles.

Assessing MSP, it was our understanding that a higher price at firm level should be reflected in the end consumer prices as well. However, what actually happens is that a higher MSP encourages farmers to prefer the impacted commodity over other substitutes. As a result, market experiences bumper production of one commodity and scarcity of others resulting in supply volatility. We therefore believe that an imbalance in production causes lower realized value as incentives are not normally distributed.

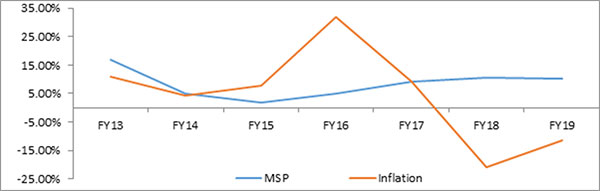

The Pulse story is a classic example of this very situation as focused Pulse cultivation incentivization has resulted in an oversupply of the otherwise highly inflationary commodity. As MSP for the commodity rose, by Q3 FY18, the inflation rate declined to -19% and remained in negative trajectory - averaging -15% over the last three quarters. Government should thus be cautious about the adverse impact of higher MSP on the overall agro commodity market atleast from the supply side perspective.

Since we believe that a more holistic approach must involve the demand side as well given the fact that the prices are ultimately determined by the level of consumption - we focused on the agro based industries for the study. In identifying the true nature of demand, agro based industries play a key role and that was our central thesis. However, no separate data base for measuring the performance of such industries is currently available since the IIP is sector agnostic. Therefore, we have devised an index to figure out the performance of these industries as their forward and backward linkages can confirm demand trends helping in anticipating prices.

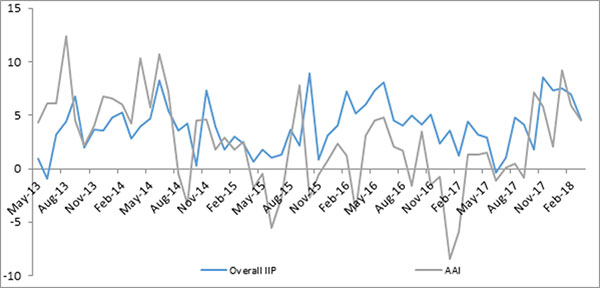

The agro index shows that after a sharp contraction during November, 2016 to February, 2017, the overall agro based industry is in somewhat recovery mode but has on average significantly undercut the IIP’s otherwise robust performance. Even though our index is now converging, it is clear that agro based industries (including food processing) were operating at sub optimal levels since FY15- even though the MSP actually shot up significantly. Pulses based industry is a special mention as such processing industries underperformed despite a rise in MSP. The revised MSP oversupplied the market with the commodity, reducing realizable price for not only the cultivators (farmers) but the processors (and forward linked supply chain) as well. Even though, our assessment is in a nascent stage at this time and we wait for Kharif data for validation - we estimate that the current rise in MSP may not substantially increase agro industry performance in the medium to long term. The cultivators not being able to realize their promised price is another concern, but is on the supply side.

Correlation between MSP, inflation and production of pulses:

| First variable | MSP-Inflation | MSP-Production | Production-Inflation |

| No lag | -0.24 | 0.23 | -0.08 |

| With one period lag MSP | -0.41 | 0.00 | -0.82 |

| With one period lead MSP | -0.07 | 0.04 |

Trend in inflation rate for major agro commodities:

MSP’s impact on Pulse Inflation

Performance of Acuité Agro Industry Index:

Annual growth (YoY):

| Acuité Agro index | IIP | Food | Textile | |

| FY14 | 5.4% | 3.3% | 1.2% | 4.2% |

| FY15 | 3.9% | 4.0% | 6.0% | 3.8% |

| FY16 | -0.3% | 3.3% | -5.6% | 2.2% |

| FY17 | 0.0% | 4.6% | -5.6% | -1.7% |

| FY18 | 3.0% | 4.4% | 8.8% | -0.3% |

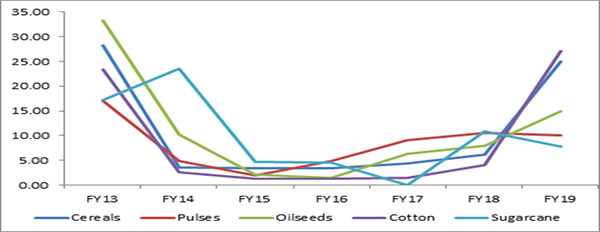

Category Wise MSP Increase

Source: Ministry of Agriculture; Acuité Knowledge Center

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD