Indian sugar industry is the second largest agro-based industry in India (as per available information in the public domain) contributing significantly towards development of rural economy. The country, in fact, is the world’s largest producer and consumer of sugar with expected production of 33 million tonnes per annum (mtpa) (~15% of the global production) and consumption of 26 mtpa in 2018-19. The total revenue realization of the industry in 2018-19 SS (Sugar Season- October to September) is estimated at ~Rs. 1 lakh crore of which ~81% will be likely constituted by sugar, and ~19% by ethanol and other by products.

As per initial estimates, surplus situation in the industry continued in 2018-19 SS following last year’s trend. However, going ahead in 2019-20 SS production is expected to decline by ~15% to 28.2 million tonnes due to decline in sugar cane area in Maharashtra and Karnataka which is likely to keep domestic sugar prices under pressure. Further, higher global prices on account of deficit production is expected to boost sugar exports from India.

Price remains to be major differentiating factor in the domestic sugar industry which is highly competitive and fragmented with around 530 operational mills as on January 2019. Player’s ability to charge premium for their products is extremely constrained given the demand- supply gap. Sugar mills with large scale of operations, sufficient cane availability and better forward integration in terms of ethanol/alcohol production from molasses & power co-generation through bagasse will position themselves better to withstand cyclical downturns.

Sugar industry continues to be highly affected by government regulations in terms of availability and pricing of sugarcane, sugar trade and by-product pricing. In fact, the pricing of sugarcane is primarily influenced by government regulations rather than economics. Further, limited correlation between cane costs and sugar realizations results in high cost of production which reduces profitability of mills endangering the issue of cane price arrears to farmers. Hence, the industry is subject to a high regulatory risk.

Key Risks & Attributes

Owing to the sugar industry’s highly cyclical nature wherein a typical sugar cycle lasts for 3-5 years (assuming normal monsoons), supply-side dynamics plays a crucial role in the dynamics of the industry. During 2018-19 SS in fact, surplus production of sugar owing to higher acreage led to a decline in prices. As a result, there was a decrease in average ex-mill sugar prices to Rs. 3,065 per quintal in 2018-19 SS (till Mar) from Rs. 3,620 per quintal in 2016-17 SS.

Cane pricing also plays an important role in determining the supply situation of the industry. While central government determines fair and remunerative price (FRP), states such Uttar Pradesh (UP) also determine their own State Advised Prices (SAP) which are generally higher than FRP. On the other hand, states like Maharashtra, Karnataka and Tamil Nadu have begun using revenue sharing model where cane prices are determined as a percentage of sugar realizations.

Going forward, in 2019-20 SS, a deficit is expected in the international market after having two surplus years which is likely to shore up the sugar prices globally. Further, despite a high opening inventory in the domestic market, lower production during the same period is expected to constrain supply which is likely to support prices.

Acuité believes that demand will likely remain steady whereas production deficit in both domestic and international market will remain a key monitorable.

The domestic sugar industry is highly competitive and fragmented with 530 mills operational as on January 2019, which constraints players bargaining power. Consequently, players with large scale of operations, good supply metrics with regard to cane availability and better operational efficiencies are less exposed to risk of raw material prices thereby helping them to remain highly competitive.

Moreover, over the last decade, several industry players have also forward integrated with ethanol/alcohol production from molasses and power co-generation through bagasse thus shielding them from the sugar industry’s cyclical downturns. In fact, with the Ethanol Blending Programme, the government has a target of 10 per cent blending of ethanol with petrol by 2022 which too will push players to take up the said model.

Acuité believes that the sugar industry is competitive and fragmented thereby constraining player’s bargaining power with respect to price. However, players with forward integrated business models are relatively better positioned.

As the government determines allocation of sugarcane, and regulates cane & by-product pricing, the industry continues to face significant input risk. Consequently, FRP of sugarcane needs to move simultaneously with any rise in minimum support prices (MSP) of other competing cash crops in order incentivize sugarcane production. Further, availability of sugarcane is highly dependent on factors like climatic conditions, access to irrigation facilities, cane variety and yield per acre. A change in any of these factors poses a significant risk to the industry.

As on March 31, 2019, sugarcane arrears were recorded at about Rs. 30,000 Cr. which further discourages farmers to continue sugarcane production as it largely impacts their working capital and cash availability for future production. Despite, the government's effort to provide soft loans to sugar mills to assist them in clearing arrears of cane growers, arrears will continue to impact the industry untill the cane prices are not entirely linked to sugar realisations.

>Acuité believes that the industry is exposed to high input risk owing to lack of control on sugarcane procurement and pricing which can be a deterrent for the sector.

The measures taken by both central and state governments continue to pressurize sugar manufacturer’s financial performance.

The industry continues to remain highly regulated in terms of allocation of sugarcane, cane pricing and by-product pricing. The central government regulates FRP for sugarcane and levies import-export duty to maintain sugar availability in the country whereas state governments also determine their own FRPs called State Advised Prices (SAP). Sometimes SAPs are higher than ex-mill prices which leads to lower profitability and higher cane arrears. Going ahead, deregulation of cane prices can be a key determinant for the industry to realise its full potential.

Acuité believes that the industry remains significantly regulated in terms of sugarcane pricing, and government measures towards sugarcane farmers will continue to impact financial performance of sugar manufacturers. Thus, we put regulatory risk highly unfavorable for the industry.

Technology obsolescence is not a major risk for the Indian sugar industry relative to other factors. With the sugar manufacturers deriving revenues from sugar sales and by-products like molasses, going ahead however, to remain competitive and achieve better product realisations, players might require to invest in technology upgradation primarily in areas like ethanol. In fact, with the Ethanol Blending Programme, the government has a target of 10 per cent blending of ethanol with petrol by 2022 which can lead players to invest in the said model.

However, technology is not a major threat to the overall profitability of the industry.

Acuité believes that the technological risk remains low for players in the sugar industry.

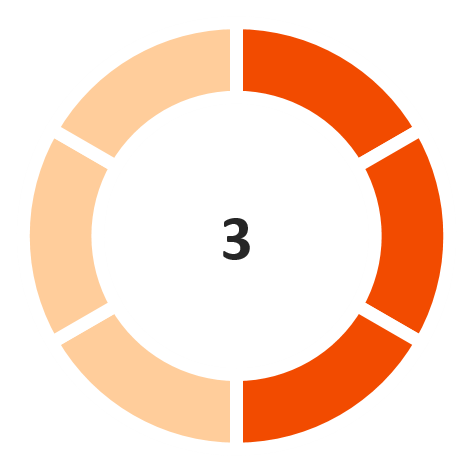

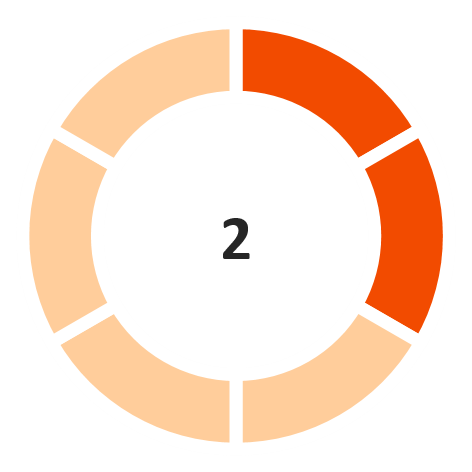

Operating Margin

(Marginally favorable)

Interest Coverage Ratio

(Marginally favorable)

Return on capital employed

(Marginally unfavorable)

Debt/ Equity

(Marginally unfavorable)

GCA days

(Unfavorable)

Note: The industry financial performance risk score is provided on a 6-point scale

Disclaimer:

Acuité IRS should not be treated as a recommendation or opinion that is intended to substitute for a financial adviser's or investor's independent assessment of whether to buy, sell or hold any security of any entity forming part of the industry.

Acuité IRS is based on the publicly available data and information and obtained from sources we consider reliable. Although reasonable care has been taken to ensure that the data and information is true,

Acuité, in particular, makes no representation or warranty, expressed or implied with respect to the adequacy, accuracy or completeness of the information relied upon.

Acuité is not responsible for any errors or omissions and especially states that it has no financial liability whatsoever for any direct, indirect or consequential loss of any kind arising from the use of Acuité IRS.

+91 99698 98000

+91 99698 98000 info@acuite.in

info@acuite.in Follow us

Follow us +91 22 49294000

+91 22 49294000 DOWNLOAD

DOWNLOAD